Over the last six months, Revolve shares have sunk to $22.10, producing a disappointing 10.8% loss - worse than the S&P 500’s 4.1% drop. This may have investors wondering how to approach the situation.

Is now the time to buy Revolve, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons why RVLV doesn't excite us and a stock we'd rather own.

Why Is Revolve Not Exciting?

Launched in 2003 by software engineers Michael Mente and Mike Karanikolas, Revolve (NASDAQ:RVLV) is a fashion retailer leveraging social media and a community of fashion influencers to drive its merchandising strategy.

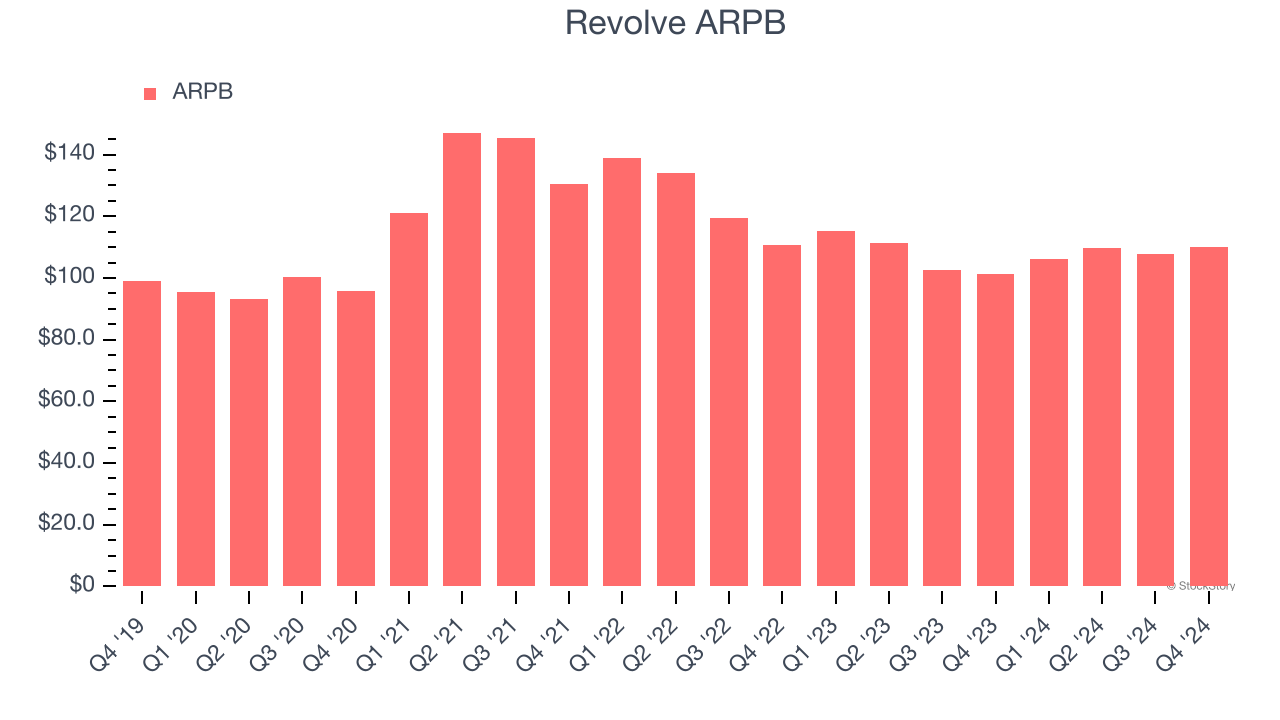

1. Customer Spending Decreases, Engagement Falling?

Average revenue per buyer (ARPB) is a critical metric to track because it measures how much customers spend per order.

Revolve’s ARPB fell over the last two years, averaging 6.6% annual declines. This isn’t great, but the increase in active customers is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Revolve tries boosting ARPB by taking a more aggressive approach to monetization, it’s unclear whether buyers can continue growing at the current pace.

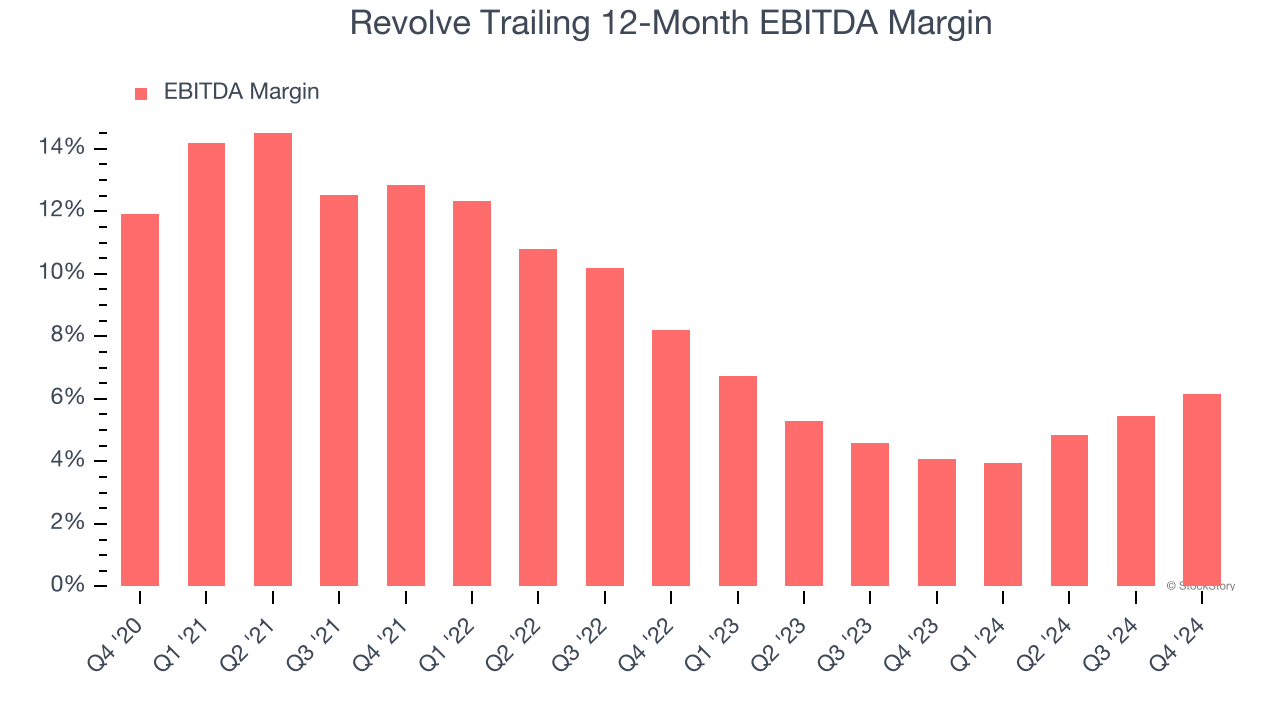

2. Shrinking EBITDA Margin

Investors regularly analyze operating income to understand a company’s profitability. Similarly, EBITDA is a common profitability metric for consumer internet companies because it excludes various one-time or non-cash expenses, offering a better perspective of the business’s profit potential.

Analyzing the trend in its profitability, Revolve’s EBITDA margin decreased by 6.7 percentage points over the last few years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its EBITDA margin for the trailing 12 months was 6.2%.

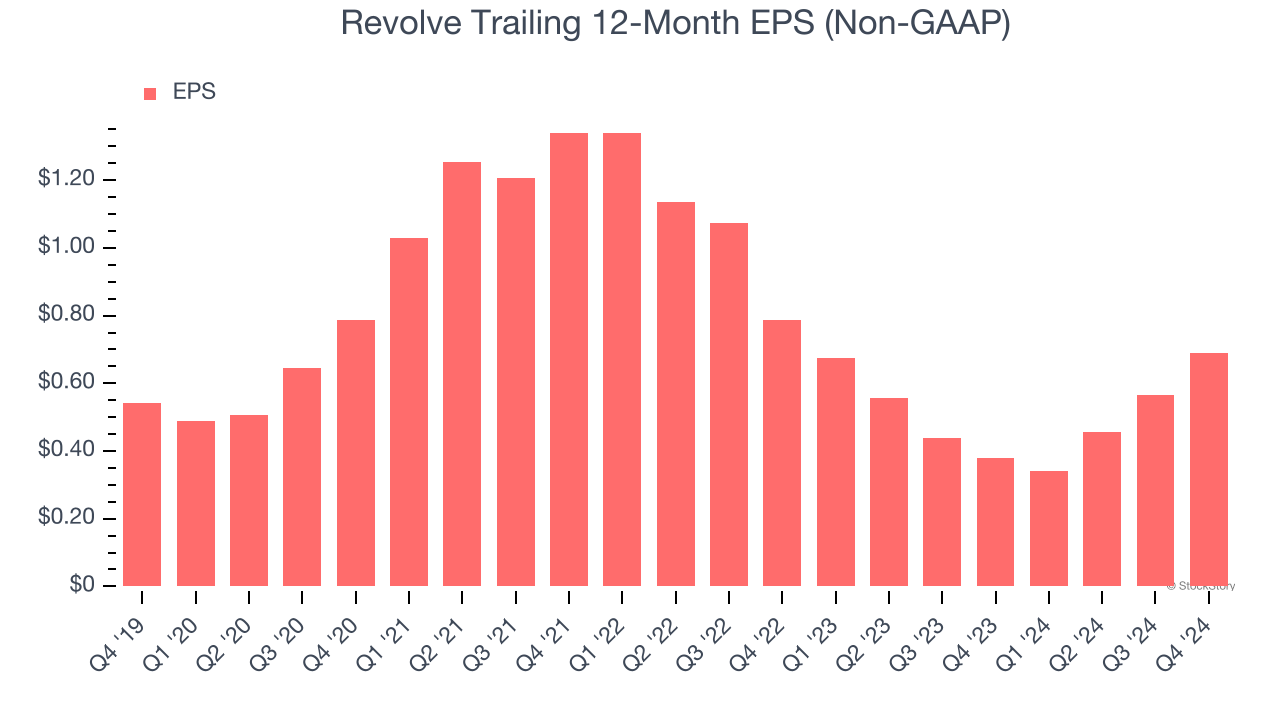

3. EPS Trending Down

We track the change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Revolve, its EPS declined by 19.9% annually over the last three years while its revenue grew by 8.2%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Revolve isn’t a terrible business, but it doesn’t pass our quality test. After the recent drawdown, the stock trades at 19.5× forward EV-to-EBITDA (or $22.10 per share). This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now. We’d suggest looking at the Amazon and PayPal of Latin America.

Stocks We Would Buy Instead of Revolve

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.